Credit Line on UPI: Unlocking New Possibilities for Small Finance Banks

Imagine a small merchant in a remote village accessing affordable credit instantly with just a few taps on their smartphone. This scenario is now a reality, thanks to the Reserve Bank of India (RBI) allowing Small Finance Banks (SFBs) to offer Credit Line on UPI. Announced during the December 2024 Monetary Policy Meet, this move significantly expands a product initially launched for Scheduled Commercial Banks in September 2023.

It paves the way for SFBs to offer pre-approved credit lines through UPI, enabling cost-efficient, accessible credit for individuals and businesses alike.

As the RBI highlighted, “This initiative has the potential to deepen financial inclusion and expand formal credit, especially for New-to-Credit (NTC) customers.”

For SFBs, this development is more than just an operational update—it’s a transformative opportunity.

Why This is Big News for Small Finance Banks (SFBs)

Reaching the Underserved

SFBs have always excelled at serving last-mile customers. Credit Lines on UPI now enable them to deepen their reach in small towns and rural areas, providing accessible and affordable credit to individuals and merchants.

New-to-Bank (NTB) Customer Acquisition

Offering low-ticket, short-tenor credit products creates a compelling entry point for NTB customers. Ideal for individuals and merchants who need quick, affordable credit without the lengthy processes of traditional lending, this opens doors to a new customer base and strengthens financial inclusion.

Cost-Efficient Operations

By integrating UPI with their existing systems, SFBs can reduce acquisition and operational costs while scaling effectively and reaching customers in even the most remote regions.

Empowering Merchants in Focused Geographies

With credit lines tied to UPI, SFBs can empower merchants across their focus geographies with easy, cost-effective access to credit, helping them grow their businesses and create local economic impact.

Whether it’s a small shop owner looking for cash flow support or a self-employed professional managing daily expenses, SFBs can become their go-to partners for growth.

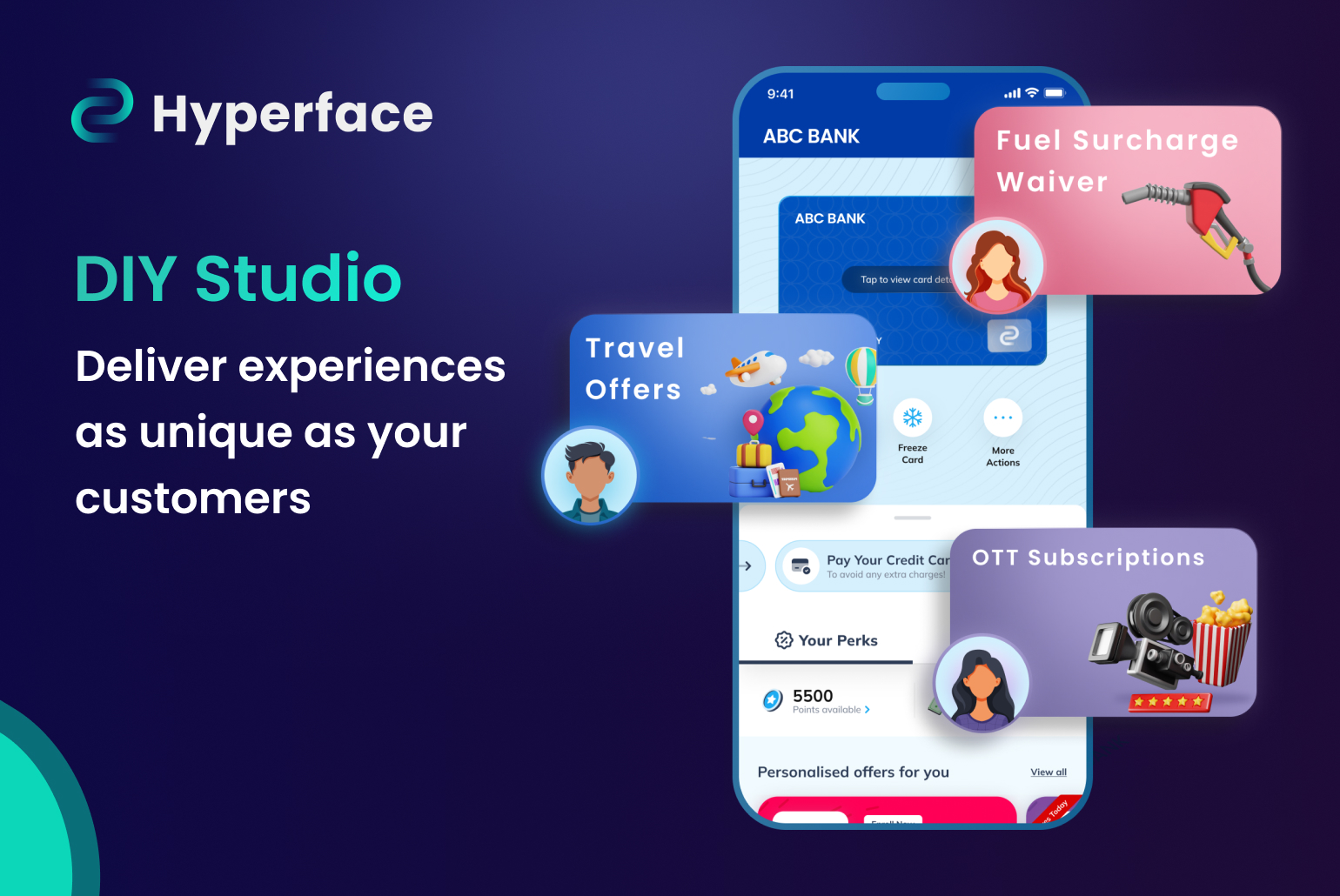

How Hyperface Enables SFBs to Unlock UPI Credit Opportunities

Hyperface’s comprehensive and modular UPI Credit Stack offers several unique benefits that empower SFBs with the tools to differentiate themselves in the market and unlock unparalleled growth opportunities:

- Experiment with Diverse Credit Programs

SFBs can quickly design and launch innovative UPI-based credit products. Features like shortened billing cycles, custom pricing, and EMI transaction splits allow SFBs to offer tailored solutions, meeting the unique needs of their customers. - Create Flexible Pricing Models

Develop dynamic pricing structures that cater to different customer profiles. With the ability to base fees on transaction logic, MCC/MID, or transaction amounts, SFBs can optimize their revenue streams while maintaining customer satisfaction. - Offer Custom Interest Rates

Hyperface enables SFBs to differentiate APRs for various customer cohorts within the same program. This flexibility ensures better customer alignment and a competitive edge. - Enhance Customer Engagement through Personalization

SFBs can use advanced segmentation to target specific customer groups with personalized offers. This includes fee waivers, strategic cross-sells, and customized nudges that enhance the user experience and drive deeper engagement. - Deploy Quickly with Brand-Aligned Solutions

With plug-and-play PWAs and SDKs, SFBs can bring UPI credit programs to market faster while ensuring a consistent brand experience for their customers. - Integrate Seamlessly with Existing Systems

Hyperface’s Switch-agnostic and CBS-compatible UPI stack ensures that SFBs can integrate with their existing infrastructure effortlessly, saving time and resources.

Looking Ahead: A New Era for SFBs

Credit Line on UPI is more than just a product—it’s a paradigm shift. SFBs now have a chance to redefine banking for millions, tapping into underserved markets and creating lasting impact.

For customers, this means easier access to credit.

For SFBs, it marks the beginning of a new era of sustainable growth.